It will come as no surprise to anyone reading this that in the dozens of calls I’ve had with credit union leaders this year, the topic of attracting and retaining deposits has come up in virtually every single one. A liquidity crunch that at first was mostly due to having investments that couldn’t be liquidated without taking a loss because of rising interest rates has turned into an all-out price war, with credit unions, banks and even tech giants trying to one-up each other by offering CDs and savings accounts at rates no one has seen for years.

Is it working? Well, as one executive whose credit union’s approach to pricing has been fairly aggressive told me recently, “Basically, any deposit growth at all was going to be the target for the year.” In other words, just not going backwards would be a success – and for many FIs, achieving even that level of “success” has been elusive.

The Numbers are Daunting

According to Callahan and Associates’ compilation of NCUA Call Report data, US credit unions saw an average increase in deposits of just 1.79 percent in the 12 month period ending June 30, 2023. That’s a little better than breaking even, but compared to the average increase of 8.35 percent in the previous 12-month period, it’s not so hot.

Now, that’s not to say that credit unions raising rates to attract deposits is all bad. In fact, it’s great for members – at least the ones who have cash – as they can finally start seeing a decent return (even if it doesn’t quite keep up with inflation). But for the credit union movement overall – well, some of the numbers are less than ideal:

- Loans are growing more than six times faster than deposits, so liquidity is tightening.

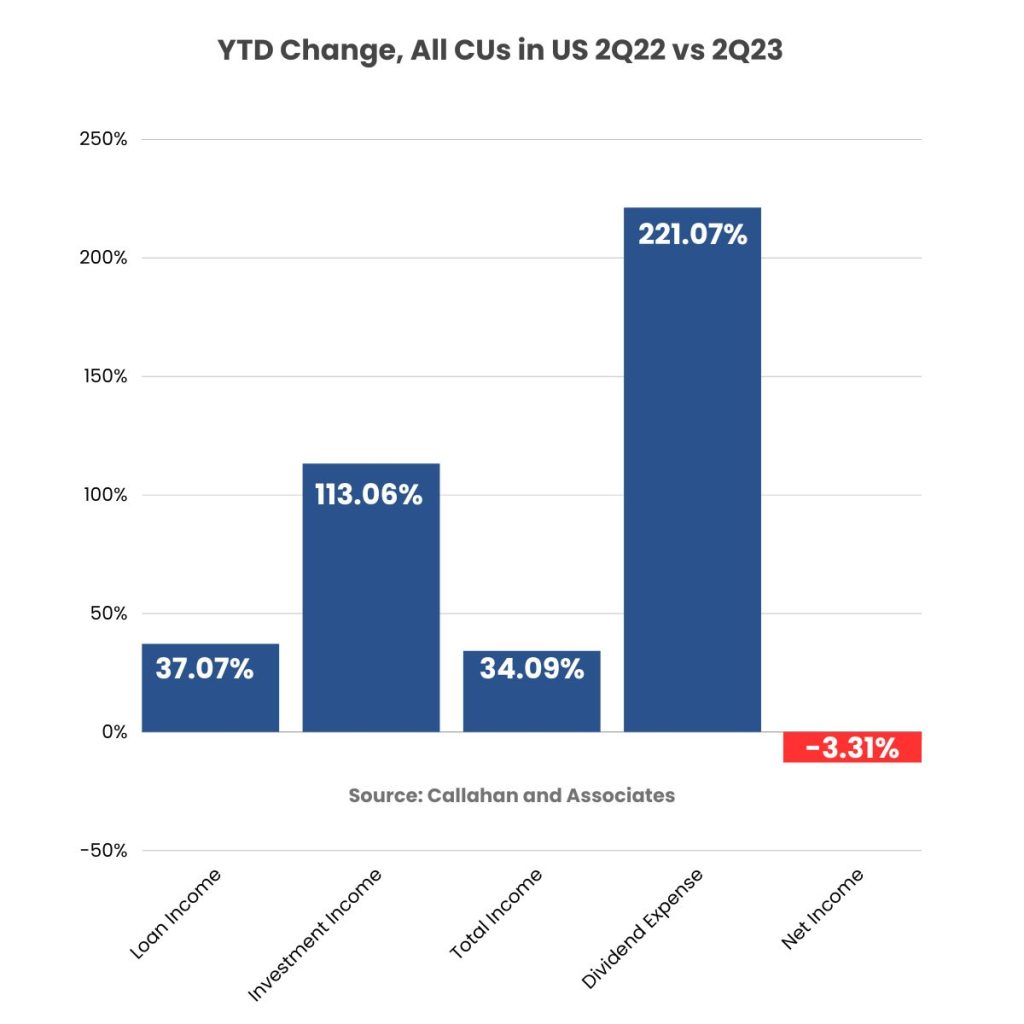

- Dividend expense YTD is up 221 percent compared to last year (and over 1,000 percent at some shops!).

- As a result, even though loan income is up 37 percent, net income is actually down YTD.

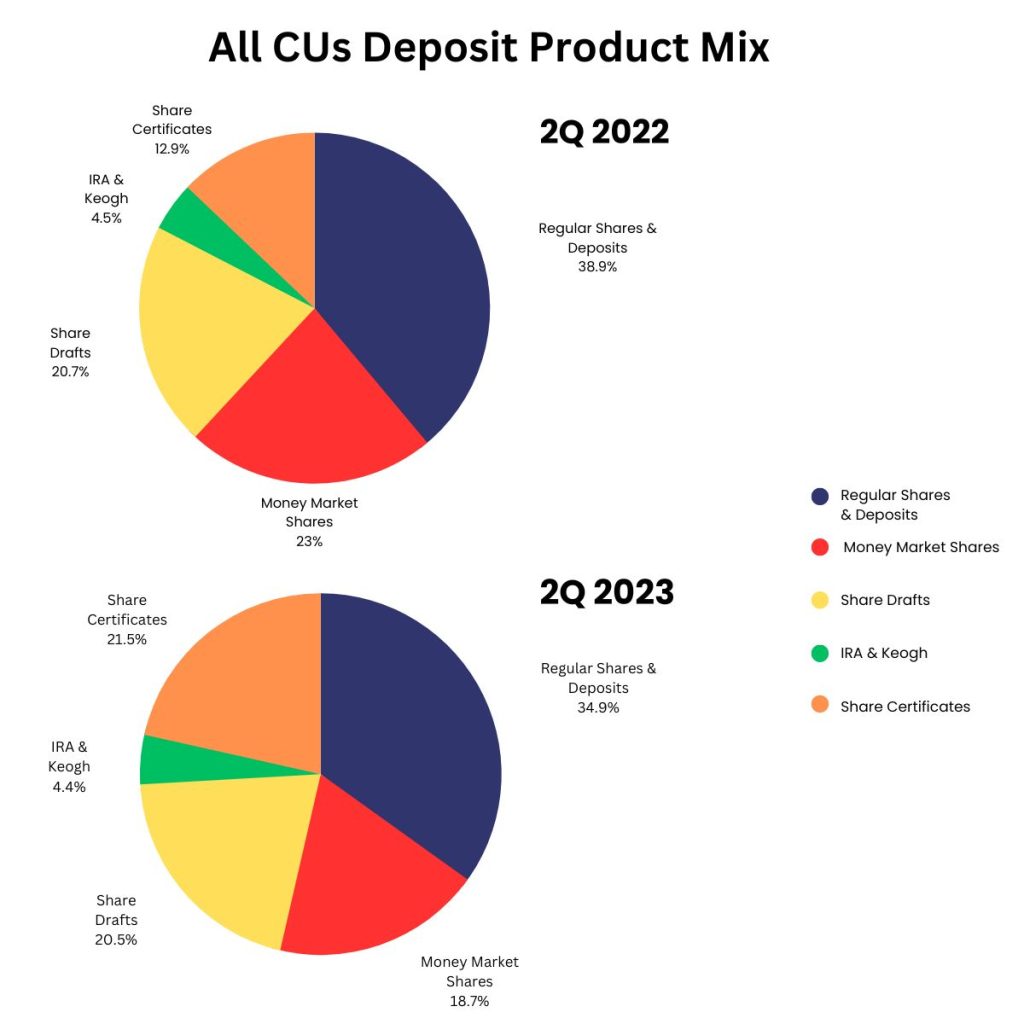

- And perhaps most telling, while the portion of total deposits held in regular shares and money markets has gone DOWN by more than eight percentage points, the portion in certificates has gone UP by even more.

YTD Change

What that last statistic tells me is that instead of those high certificate rates attracting new money, what they’re doing is enticing members to move money from core deposits – money that’s traditionally NOT rate sensitive – into the part of the portfolio with the highest cost of funds. And that, to me at least, seems like cause for concern.

Shares and Shares Alike?

Some readers might see this and say, “Sure, it’s a problem, but how can you avoid it? We post a rate, we can’t control who takes us up on it.” Some might even say to do anything different isn’t very “credit union-like” (wouldn’t be the first time I’ve been accused of that) because we treat all members the same.

On the other hand, there are plenty of experts out there (again, I’m not one) who would tell you that when it comes to deposit pricing, the last thing you should do is just post a high rate and apply it to everyone, because you’ll absolutely end up spending more than you have to. My old friend Marc Cooley, president of Kohl Analytics Group, would tell you that there’s a lot that goes into a comprehensive pricing strategy, including figuring out what’s important to each member (and it’s not always price). Sometimes, it’s not about the rate until the credit union makes it about the rate. (If you’ve never spoken to Marc or checked out Kohl’s services, you should visit kohlag.com.)

Deposit Product Mix

So, what’s a credit union to do? It’s complicated. I read a great article recently where someone with 30 years of banking experience extolled the virtues of negotiating rates with individual depositors in response to them saying they want a better return. You can visualize it, right? Member comes in, goes to the teller window or into the manager’s office and says, “I’m taking my money out unless you raise my rate to X.” Manager calls somebody in Finance, puts the member on the phone, and negotiations ensue. Rate-sensitive depositor gets what he or she needs, but the rest of the portfolio gets left alone.

Can Pricing Be Personal in a Digital World?

Sounds great, but here’s my question: How are you supposed to do that when your members don’t come into a branch? The exact numbers keep changing, but somewhere around 65 percent of consumers say they never visit a branch anymore, and around 90 percent do at least some of their banking online or in a mobile app. Instead of members demanding a higher rate and then negotiating, isn’t this a more likely scenario:

- Member sees that rates are going up.

- Member goes online to see who has the best deal.

- Member maybe checks credit union’s website to see if theirs is better.

- Member opens a certificate online wherever the best rate is and funds it from his or her credit union account.

What is the right price?

Let’s face it: The world of banking has changed, and trying to do things the way we used to doesn’t work anymore. But is the one-size-fits-all, “throw it out on the website and hope for the best” approach the only thing left in a digital world?

Unless you have mobile member engagement tools and a comprehensive strategy to use them, it might be. And that would be a real problem.

Steve Kelley is Pulsate’s Director of Business Development and has spent nearly 30 years involved in financial services marketing in one form or another. From marketing to lending to digital banking, his career has exposed him to hundreds of industry experts whose wisdom and insights have shaped his own, and he loves sharing what he’s learned and what he thinks about it.